The quick answer is yes, you can have both a 401(k) and an individual retirement account (IRA). … These plans have something in common in that they offer the opportunity for deferred tax savings (and, in the case of a Roth 401(k) or Roth IRA, tax-free income as well).

Is it better to contribute to a traditional 401k or Roth 401k?

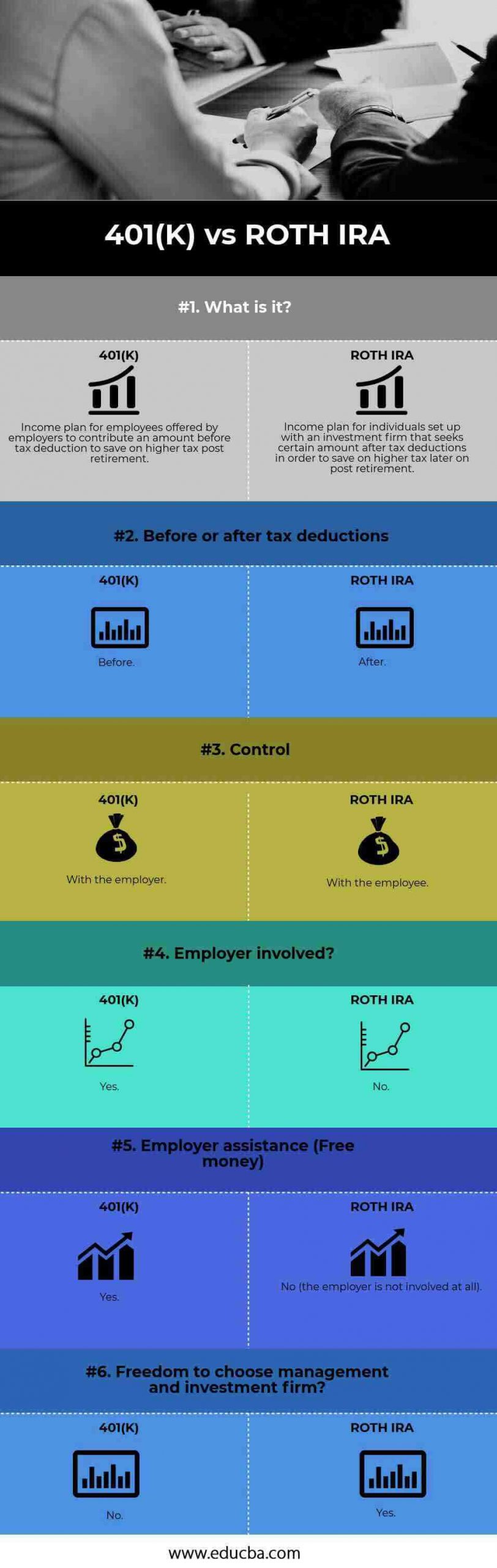

Contents

That’s because, typically, they’re currently in the low-income tax bracket, and the upfront tax deduction from a traditional retirement account is now less valuable than a tax-free Roth withdrawal down the road. Lately, however, financial advisors have been directing their older clients to Roth accounts as well.

Is it better to contribute to a 401k or a Roth? A Roth 401(k) tends to be better for those with higher incomes, have higher contribution limits, and allow for employer matching funds. Roth IRAs allow your investment to grow longer, tend to offer more investment options, and allow for easier early withdrawals.

What is the difference between a Roth 401k and a traditional 401k?

With a Roth 401(k), your money goes after taxes. That means you pay taxes now and take home a little less than your paycheck. When you contribute to a traditional 401(k), your contribution is pretax. They are taken from the top of your gross income before your paycheck is taxed.

What is the benefit of a Roth 401 K over traditional?

With a Roth 401(k) you’ll be contributing with after-tax money, so you won’t be enjoying today’s tax breaks. In exchange, the money you withdraw in retirement will be tax-free. In a Roth 401(k), you will not only enjoy tax-free growth of your investment profits, but also tax-free withdrawals.

What are the pros and cons of a Roth 401k?

Pros and Cons of a Roth 401(k)

- Excess:

- Tax free withdrawals. …

- Special situations allow penalty-free initial distribution. …

- There is no income limit. …

- Counter:

- Contributions are not tax deductible. …

- Minimum distribution required. …

- More than Personal Finance Cheat Sheets:

How does a Roth 401k work?

With a Roth 401(k), the main difference is when the IRS makes the withholding. You make a Roth 401(k) contribution with taxable money (as you would with a Roth individual retirement account, or IRA). Your income then grows tax-free, and you pay no taxes when you start taking withdrawals in retirement.

Should high earners use Roth 401k or traditional?

Roth has also been recommended as a way to diversify the tax treatment of retirement income sources and to provide retirees with tax flexibility. Even if you end up in a lower income tax bracket when you retire, withdrawals from your traditional retirement account could potentially put you into a higher tax bracket.

Should I do all Roth or traditional 401k?

If you expect to be in a lower tax bracket in retirement, a traditional 401(k) may make more sense than a Roth account. But if you’re in a lower tax bracket now and believe you’ll be in a higher tax bracket when you retire, a Roth 401(k) may be a better choice.

Does it make sense to have a Roth and traditional 401k?

If you’ve funded a traditional 401(k), it makes sense to add a Roth plan to the mix. It’s actually worth it not to keep all your eggs in one retirement basket, even if it makes the most financial sense right now. That’s because having both plans will give you flexibility later.

Is a Roth 401k good for high earners?

Choosing an Account for the High-Income With the potential for large compound growth, along with the benefits of this non-taxable money, the Roth 401k can be a great choice for high-income earners.

Can I contribute to both a 401k and a Roth 401k?

If your employer offers a 401(k) plan, there may still be room in your retirement savings for a Roth IRA. Yes, you can contribute to 401(k) and Roth IRAs, but there are certain limitations you should consider. This article will cover how to determine your eligibility for a Roth IRA.

Do Roth 401k contributions count towards 401k limit?

You make a designated Roth contribution to a separate Roth account from your 401(k) plan. They count to the limit.

What is the max I can contribute to my 401k and Roth 401 K?

The overall Contribution Revenue limit for a Roth 401(k) cannot exceed your compensation, of course. For 2021, the combined total of employee and employer contributions must not be less than $58,000 ($61,000 for 2022) or 100% of the employee’s salary, and $64,500 ($67,500 for 2022) if you are 50 years old or older.

How much can I contribute to my 401k and Roth 401k in 2020?

The Roth 401(k) contribution limit for 2020 and 2021 is $19,500, but those aged 50 and over can also make an additional $6,500. Employers can contribute to Roth 401(k)s employees through match or elective contributions.

When would you not want a Roth IRA?

For 2020, sole taxpayers cannot contribute to Roth if they earn $139,000 or more. Your contribution is reduced if you earn between $124,000 and $139,000. For 2021, the income limit has been increased. Roth IRA contributions from singles are prohibited if your income is $140,000 or more in 2021.

When can you not have a Roth IRA? There is no age limit or limit for making a Roth IRA contribution. For example, a teenager with a summer job could found and fund Roth. (May have to custodial account if they are minors.)

Is a Roth IRA ever a bad idea?

A Roth IRA isn’t necessarily a bad idea if you qualify for a suitable employer through your employer’s workplace retirement plan, but it’s not a great first choice. … You can contribute up to $19,500 for a 401(k) in 2020 or $26,000 if you are 50 or older, compared to just $6,000 and $7,000, respectively, for a Roth IRA.

Can you lose all your money in a Roth IRA?

In the same way, if you invest all of your Roth IRA money in one stock, and the company goes bankrupt, there’s a good chance you could lose all your money. Even a properly diversified stock portfolio can lose most of its value in a short period of time during bad economic conditions.

Why a Roth IRA is a bad idea?

The main loss of a Roth IRA contribution is made in after-tax money, which means there is no tax deduction in the year of contribution. Another drawback is that withdrawals must not be made before at least five years have passed since the first contribution.

Are ROTH IRAs still a good idea?

If you are already earning and meeting your income limit, a Roth IRA can be an excellent tool for retirement savings. But keep in mind that it is only one part of an overall retirement strategy. If possible, it’s a good idea to contribute to other retirement accounts as well.

Why should I not get a Roth IRA?

Roth IRAs offer several key benefits, including tax-free growth, tax-free withdrawals in retirement, and no minimum distribution required. The obvious disadvantage is that you’re donating post-tax money, and that’s a bigger hit on your current income.

Are Roth IRAs still a good idea?

A Roth IRA or 401(k) makes the most sense if you believe you will earn more in retirement than you are earning now. If you expect your income (and tax rate) to be lower in retirement than you currently are, a traditional account is likely a better bet.

What are the disadvantages of a Roth IRA?

Cons of Roth IRA

- You pay taxes up front.

- The maximum contribution is small.

- You have to set it yourself.

- There is an income limit.

- Your savings grow tax free.

- No need for the required minimum distribution.

- You can withdraw your contribution.

- You get tax diversification in retirement.

What are the disadvantages of a Roth IRA?

Cons of Roth IRA

- You pay taxes up front.

- The maximum contribution is small.

- You have to set it yourself.

- There is an income limit.

- Your savings grow tax free.

- No need for the required minimum distribution.

- You can withdraw your contribution.

- You get tax diversification in retirement.

Can you lose money in a Roth IRA?

Yes, you can lose money in a Roth IRA. The most common causes of losses include: negative market fluctuations, early withdrawal penalties, and insufficient amount of time to combine. The good news is, the more time you let your Roth IRA grow, the less likely you are to lose money.

What are the good and bad of Roth IRA?

Roth IRAs may seem ideal, but they have their drawbacks, including a lack of direct tax deductions and a low maximum contribution. The investment information provided on this page is for educational purposes only. In the world of retirement accounts, the Roth IRA is the child of choice. …

What is a backdoor Roth?

A backdoor Roth IRA is not an official type of individual retirement account. Instead, it’s the informal name for a complicated Internal Revenue Service (IRS)-approved method for high-income taxpayers to fund Roths, even if their income exceeds the IRS-allowed limit for regular Roth contributions.

Is a backdoor Roth a good idea? A Backdoor Roth IRA is worth considering for your retirement savings, especially if you are on a high income. A Backdoor Roth conversion can be something to consider if: You’ve made the most of other retirement savings options. Willing to leave money on Roth for at least five years (ideally longer!)

What is the purpose of a backdoor Roth?

The Roth IRA backdoor is a way for people with high incomes to circumvent Roth’s income limits. Basically, a backdoor Roth IRA boils down to some fancy paperwork: You put money into a traditional IRA, convert your contribution funds into a Roth IRA, pay some taxes and you’re done.

Why is a backdoor Roth a good idea?

In particular, when it comes to Roth IRAs, one of the biggest benefits is that they allow eligible investors to enjoy tax-free withdrawals of their money. The Roth IRA backdoor allows people with high incomes to circumvent Roth’s income limits.

Do you have to do a backdoor Roth every year?

If your income is too high, you can’t contribute directly to a Roth individual retirement account, but you can get it backdoor. …Repeat every year, and you can collect a nice retirement cat.

Is backdoor Roth still allowed in 2020?

You have until the federal tax filing deadline for each tax year to make an IRA contribution. … If you haven’t filed your taxes for 2019, you have until April 15, 2020, to complete a backdoor Roth IRA conversion.

How much does it cost to backdoor a Roth?

You are allowed to contribute less than your earned income or $6,000 in a traditional IRA, which can then be converted into a backdoor Roth IRA. If you are 50 years or older, you can also make an additional $1,000 each year.

Can I do backdoor Roth every year?

Did you know that there is a way to get up to $56,000 into your Roth IRA annually even if the contribution limit is $6,000 per year? Dubbed the “Mega Backdoor Roth,” this strategy allows taxpayers to increase their annual contribution to their Roth IRA by $56,000 (for 2019).

Is backdoor Roth still allowed in 2021?

A Roth mega backdoor allows people to save up to $38,500 in a Roth IRA or Roth 401(k) in 2021 or $40,500 in 2022. But not all 401(k) plans allow it.

Is backdoor Roth still allowed in 2021?

A Roth mega backdoor allows people to save up to $38,500 in a Roth IRA or Roth 401(k) in 2021 or $40,500 in 2022. But not all 401(k) plans allow it.

Is the backdoor Roth allowed in 2022?

Starting in 2022, the bill proposes to block the conversion of Roth backdoors. You will no longer be able to convert after-tax savings in your 401(k) or Traditional IRA to a Roth IRA, which will terminate the backdoor Roth conversion.

Can you still do a backdoor Roth IRA in 2021?

Single filers with modified adjusted gross income (MAGI) for 2021 equal to or above $140,000, or $208,000 for couples filing together, cannot contribute directly to a Roth IRA – but they can still take advantage of this special account by opening through ‘back door.

Are backdoor Roth IRAs still legal?

Removal of Backdoor Roth IRA and Mega Backdoor Roth IRA. Effective 2022, after-tax amounts in an IRA cannot be converted to a Roth IRA. This rule will apply to all taxpayers regardless of their adjusted gross income level. … The bill would also eliminate after-tax contributions for eligible plans.

Comments are closed.